The sharp reversal in global equity markets in April posed a familiar challenge for quantitative hedge funds as markets did a flip from crisis mode to a more optimistic view faster than most models are designed to adapt.

The PivotalPath Equity Quant Index rose 0.9 percent last month. While that performance was a tiny fraction of the gains for directional equity strategies, the fact that quants finishing the month in positive territory was a good signal of the funds' resilience.

Every month Institutional Investor publishes a subset of hedge fund indices from PivotalPath. Scroll to the end of the article to see additional categories.

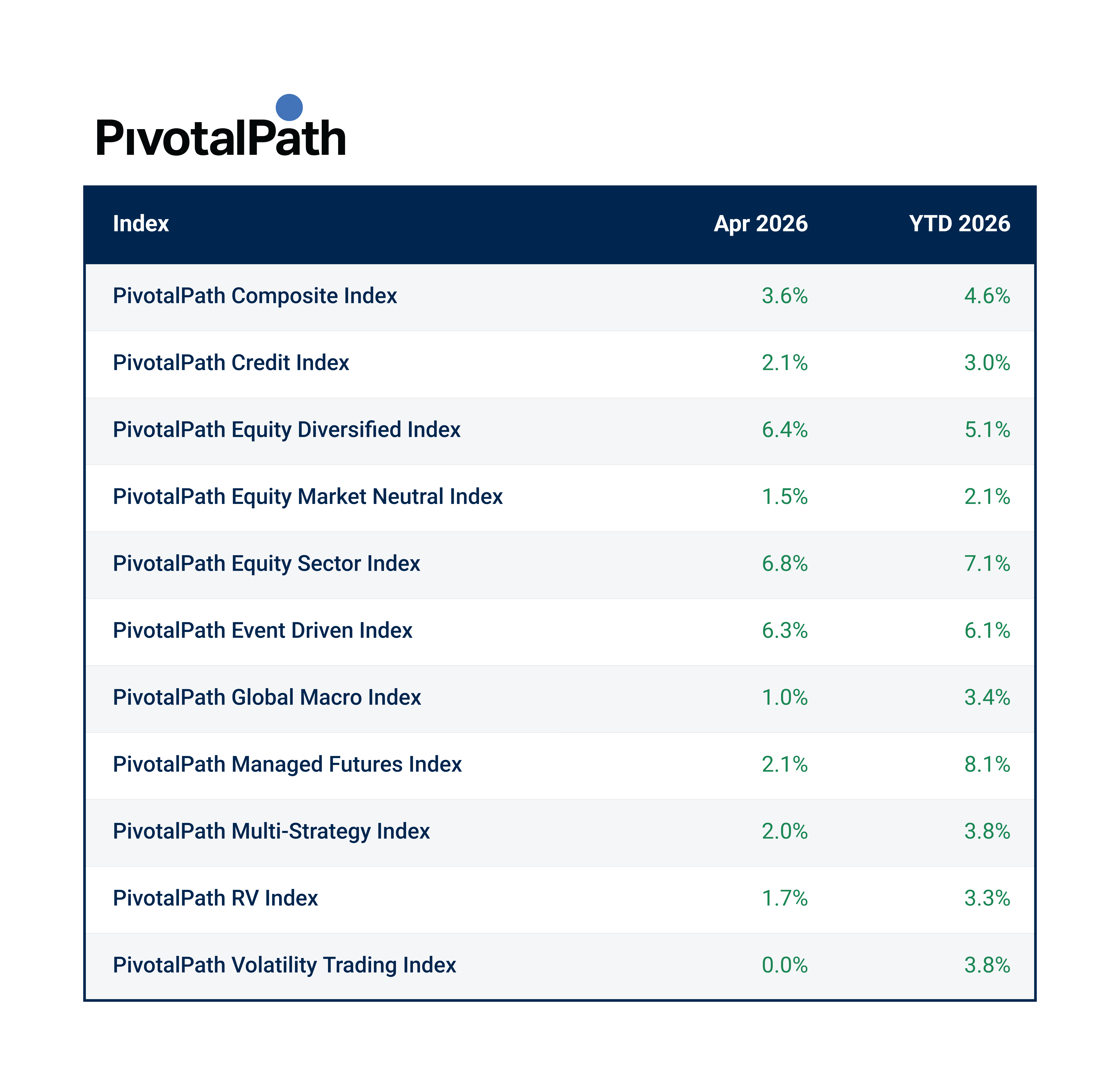

For hedge funds broadly, the rally made for a strong recovery month. PivotalPath’s Composite Index gained 3.6 percent in April (it’s up 4.6 percent for the year) and its equal-weighted Composite climbed 5.1 percent, a good indication that hedge funds of all sizes, not just the largest firms, delivered healthy returns.

April was the mirror image of March, when the spike in global oil prices after the U.S. and Israeli attack on Iran sent stocks tumbling and drove many systematic strategies into defensive positioning. But a month later, equities rebounded sharply after news of a U.S.–Iran ceasefire, however fragile, and the subsequent unwinding of hedges, a rally in AI-related stocks, and capital flowing back into Asia, with the exception of Japan.

(Click here for the latest index performance data and access to PivotalPath's full suite of hedge fund indices.)

Not surprisingly, equity hedge funds were strong performers. PivotalPath’s Equity Diversified Index surged 7 percent in April, while equity sector strategies gained 6.8 percent and event driven funds returned 6.9 percent as managers quickly moved from hedging a crisis to taking on risk.

Hedge funds in Asia were the biggest winners in April. The Equity Diversified: Asia Long/Short Index increased 9 percent, delivering an outsized rebound after the region had driven disproportionate losses a month earlier. In March, Taiwan and Korea longs accounted for roughly 20 percent of global long portfolio losses despite representing only about 7.5 percent of gross exposure. Funds that maintained conviction in those positions — or added amid the drawdown — captured significant upside as sentiment reversed.

Lower-beta and diversifying strategies struggled to keep pace with the equity snapback but remained modestly positive. Credit strategies returned 1.3 percent, Equity Market Neutral gained 1.4 percent, Global Macro rose 1.0 percent, and Multi-Strategy funds added 1.6 percent. For many of these strategies, April highlighted the difficulty of competing with surging equity markets while maintaining defensive mandates.